For More Free Videos, Subscribe to the Rhodes Brothers YouTube Channel.

You could be losing thousands of dollars from your investments and not even know it. That’s not an exaggeration—it’s a reality for many investors who overlook one critical factor: fees and expenses.

Whether you’re a first-time investor or have been in the market for years, understanding how investment fees affect your returns could be the difference between building real wealth and just treading water. And the worst part? These fees are often hidden in plain sight—camouflaged in fine print or buried under complicated jargon.

In this post, we’re going to break it all down in plain English. You’ll learn:

- What types of fees most investors pay (often unknowingly)

- How these fees eat into your compounding growth

- Real-life examples comparing different investment options

- Actionable steps to reduce fees and maximize returns

- Mistakes to avoid that could cost you tens of thousands over time

As John S. Rhodes of the Rhodes Brothers Channel put it:

“Fees are insidious. It’s a tapeworm that eats away at your investment return.”

And he’s absolutely right. By the end of this article, you’ll be equipped with the knowledge and tools to ensure you’re keeping more of your hard-earned money, not handing it over in silent bites to someone else.

Let’s dive in.

TL;DR

- Investment fees can eat up 25-40% of your gains over time.

- Understand expense ratios, management fees, and transaction costs.

- Compare similar investments—not all funds are created equal.

- Use low-cost index funds and ETFs to minimize fees.

- Leverage tools like Personal Capital, Morningstar, and brokerage fee analyzers.

- Avoid actively managed funds with high fees unless they consistently beat the market (most don’t).

- Take control today—shop around, ask questions, and dig into the fine print.

How Fees and Expenses Erode Investment Returns

Even the smartest investment strategy can fall short if you’re paying too much in fees. It’s like trying to fill a bucket with a hole in the bottom—the more you pour in, the more leaks out. What many investors don’t realize is that seemingly small fees, when compounded over time, can take a massive bite out of your returns. In fact, they’re often the #1 silent killer of long-term wealth.

Why Fees Matter More Than You Think

Here’s the hard truth: when it comes to investing, it’s not just about what you earn—it’s about what you keep.

Even a small fee difference, like 1%, can cost you tens of thousands of dollars over 10–20 years. Why? Because fees compound just like gains—but in reverse. Every dollar paid in fees is one less dollar that can compound for you.

“Compound interest is the eighth wonder of the world. He who understands it, earns it… he who doesn’t… pays it.” – Albert Einstein

The Big Three: Common Investment Fees

Let’s break down the most common types of fees and how they impact your returns:

1. Expense Ratios

This is the annual fee charged by mutual funds and ETFs, expressed as a percentage of your investment. For example:

- Actively managed fund: 1.25%

- Low-cost index fund: 0.04%

A 1.21% difference may not seem like much—but on a $100,000 investment over 20 years, it could cost you over $30,000.

2. Management Fees

Charged by financial advisors, typically 1% annually. If your advisor isn’t outperforming the market, this fee can drag down your returns significantly.

3. Transaction Fees

Every time you buy or sell, some platforms may charge. While many brokers now offer commission-free trading (like Robinhood or Fidelity), some funds still charge load fees or hidden costs.

The Power of Comparison: Real-Life Example

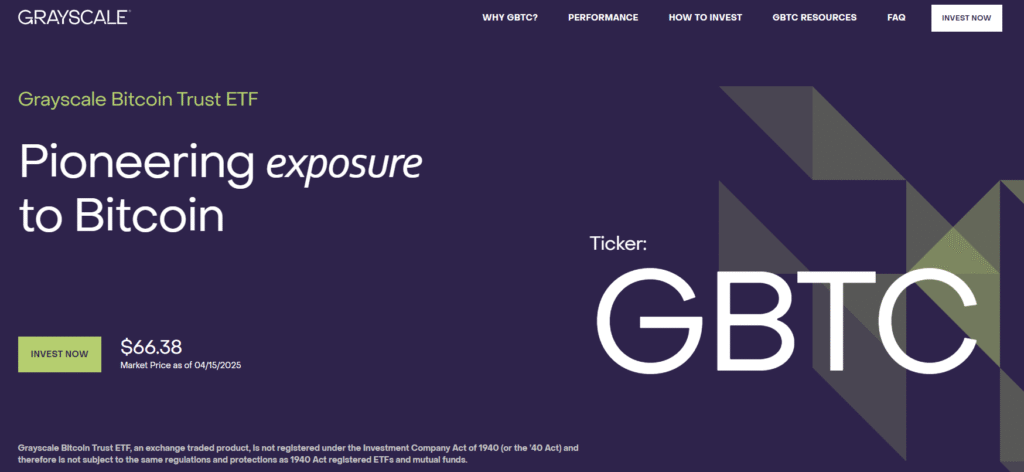

Let’s say you’re investing in Bitcoin through an ETF. You have two options:

- GBTC (Grayscale Bitcoin Trust): Fee ~1.5%

- IBIT (BlackRock Bitcoin ETF): Fee ~0.25%

Over 10 years, assuming a 7% annual return:

- $10,000 in GBTC would grow to ~$17,100

- $10,000 in IBIT would grow to ~$19,300

That’s a $2,200 difference just from picking a lower-fee fund. Same asset. Same risk. Wildly different outcome.

Actionable Steps to Reduce Investment Fees

Fees are one of the few aspects of investing you can control. While you can’t predict market returns, you can choose how much you’re willing to pay to invest your money. Reducing fees is one of the most effective ways to boost your net returns—without taking on more risk.

Here’s how to take control, broken down by experience level and life stage:

For Beginners: Build the Right Foundation

If you’re just starting out, the most important move is to keep it simple and low-cost. You don’t need to know everything—just enough to avoid the most common traps.

Actionable Tips:

- Use Broad-Market Index Funds

Start with low-cost, diversified index funds like:- Vanguard Total Stock Market ETF (VTI) – Expense Ratio: 0.03%

- Fidelity ZERO Total Market Index Fund (FZROX) – Expense Ratio: 0%

These funds give you exposure to the entire U.S. stock market with minimal cost.

- Avoid “Load” Fees

Stay away from mutual funds that charge front-end or back-end “loads.” These are basically sales commissions that reduce your investment before it starts growing. - Use Commission-Free Brokers

Platforms like Fidelity, Schwab, Vanguard, and Robinhood offer $0 trade commissions. This means you invest $100, and all $100 goes to work for you. - Educate Yourself with Free Resources

Don’t pay for what you can learn for free. Check out:- Bogleheads.org

- Investopedia’s Investing 101

- The Rhodes Brothers YouTube Channel for practical investing breakdowns

For Millennials: Automate and Optimize

Millennials are in the sweet spot of investing—young enough to benefit from compounding, but experienced enough to optimize. The key here is automation and cost-efficiency.

Actionable Tips:

- Use Low-Fee Investment Apps

Platforms like M1 Finance, SoFi Invest, or Public offer fractional shares, automated rebalancing, and no commissions. - Embrace Passive Investing

Focus on passive ETFs that track the market instead of chasing individual stocks or flashy funds. Examples include:- SCHB (Schwab U.S. Broad Market ETF) – Expense Ratio: 0.03%

- ITOT (iShares Core S&P Total U.S. Stock Market ETF) – Expense Ratio: 0.03%

- Robo-Advisors (With Caution)

Services like Betterment and Wealthfront offer hands-off investing with smart portfolio management. Most charge 0.25% annually, but always check the total cost (including fund fees). - Avoid Overlapping Funds

Don’t buy multiple ETFs that all hold the same stocks. This leads to redundancy and unnecessary fees. Use tools like Morningstar Portfolio X-Ray to see what’s really inside your portfolio.

For Those Nearing Retirement: Cut the Fat, Not the Growth

As you approach retirement, every percentage point matters. You’re closer to needing your money, so preserving capital and minimizing drag from fees is crucial.

Actionable Tips:

- Consolidate Old Accounts

Roll over old 401(k)s and IRAs into one or two low-cost providers. This makes it easier to manage and ensures you’re not paying multiple layers of fees. - Work with a Fee-Only Advisor

Instead of paying 1% of your assets every year, hire an advisor who charges a flat fee or hourly rate. Look for professionals who hold a fiduciary duty, meaning they’re legally required to act in your best interest. - Review and Rebalance Annually

Use this time to:- Reduce exposure to high-fee funds

- Shift into more conservative, low-cost investments

- Rebalance using commission-free trades

- Use Retirement Planning Tools

Services like Personal Capital offer free retirement planners and fee analyzers. These tools show how much you’re paying in fees and how much that may cost you over time.

Common Mistakes to Avoid

Even seasoned investors fall into traps that quietly eat away at their profits. The reality is that small oversights can lead to big losses—especially when they go unnoticed for years. Let’s take a deeper look at the most common mistakes investors make regarding fees and expenses, and more importantly, how to avoid them.

Ignoring Expense Ratios

Many people assume that all ETFs and mutual funds are inexpensive just because they’re labeled as “index” or “passive.” But that’s not always the case.

Some ETFs—especially those that are sector-specific, thematic, or actively managed ETFs in disguise—carry expense ratios closer to 0.75% or even 1%. That may not sound like much, but over a 20–30 year investing horizon, that small percentage can translate to tens of thousands of dollars in lost returns.

What to do instead:

- Always verify the fund’s expense ratio before buying. Use tools like Morningstar, ETF.com, or your brokerage’s fund screener.

- Stay under 0.10% for broad-market ETFs, and be wary of anything above 0.50% unless you’re confident in the added value.

Paying for Underperformance

One of the most frustrating mistakes investors make is paying a premium for poor results. Actively managed mutual funds often charge 5 to 20 times more in fees than passive alternatives, yet fail to outperform them consistently.

For example, the SPY ETF, which tracks the S&P 500, has an expense ratio of 0.09%. Many actively managed large-cap funds charge 1% or more, yet don’t consistently beat SPY after fees.

Why this happens:

- You’re paying for “expertise,” but market timing and stock picking rarely beat a diversified index.

- Managers churn portfolios, adding higher internal trading costs that further erode returns.

What to do instead:

- Compare the historical performance of active funds to a relevant benchmark, like SPY or VTI.

- If an active fund doesn’t outperform after fees, it’s probably not worth it.

- Look for actively managed funds with a long-term track record and lower-than-average fees if you want to mix styles.

Not Reviewing Regularly

Investments are not “set it and forget it.” While long-term investing is smart, neglecting your portfolio altogether can be costly.

Here’s why:

- Expense ratios and fund structures change. A low-cost fund today could increase fees tomorrow.

- Some funds undergo management changes or merge, altering their risk level, holdings, and costs.

- Your portfolio may become overweight in certain sectors, increasing your risk profile unintentionally.

What to do instead:

- Conduct a yearly portfolio review. Use this time to:

- Check for fee increases

- Rebalance your allocations

- Replace underperforming or high-cost funds

- Use tools like Personal Capital, Morningstar Portfolio Manager, or your brokerage’s analysis dashboard to stay on top of changes.

Assuming Robo-Advisors Are Always Cheap

Robo-advisors offer convenience, automatic rebalancing, and tax-loss harvesting—but they’re not always the lowest-cost option.

Most robo-advisors charge a management fee of 0.25%, which sounds low. However, they also invest in ETFs that may carry additional expense ratios, usually between 0.07% and 0.15%. This means your true annual cost could be 0.32% to 0.40%, which is 3–4 times higher than building your own index fund portfolio.

Also, some robos upsell premium services—like access to human advisors—for an extra fee, often 0.40% to 0.50% or more.

What to do instead:

- Ask yourself: Are you paying for automation, or could you do it yourself?

- Compare the all-in cost (management fee + fund fees) to a DIY portfolio of ETFs like:

- VTI (Vanguard Total Market)

- BND (Vanguard Total Bond)

- VXUS (Vanguard Total International)

- For hands-off investors, robos are fine—but don’t assume they’re always the cheapest option.

Frequently Asked Questions

How do I check the fees on a mutual fund or ETF?

Use sites like Morningstar, your brokerage’s fund profile page, or tools like Personal Capital to see the expense ratio and other hidden costs.

What is a good expense ratio?

For index funds and ETFs: Under 0.10% is excellent. Actively managed funds should be under 1%, but even then, be cautious.

Are robo-advisors worth the fee?

They can be for beginners, but always compare the total cost (advisory + underlying fund fees) to a DIY index portfolio.

Do fees really matter for small portfolios?

Yes! Even if you’re investing $1,000, high fees can stunt your growth. Starting small with low fees is better than growing a high-fee habit.

How do financial advisors get paid?

Some charge a flat fee, others a percentage of your assets (AUM), and some earn commissions. Fee-only advisors are usually more transparent.

Should I avoid all actively managed funds?

Not necessarily, but be cautious. Most don’t beat the market. If you find one with a solid track record after fees, it may be worth it.

What’s the difference between front-end and back-end loads?

Front-end = fee when you buy. Back-end = fee when you sell. Avoid funds with either unless there’s a clear advantage elsewhere.

Are index funds safe?

They’re diversified and low-cost, making them ideal for long-term investors. They track the market, so you won’t beat it—but you won’t lag behind either.

How often should I review my fees?

At least once a year. Use that time to rebalance, check for hidden costs, and make sure your investments still align with your goals.

Can I negotiate advisor fees?

Yes! Some advisors will work on flat fees, hourly rates, or even reduce their AUM percentage for larger portfolios.

Keep More of What You Earn

Fees might not seem like a big deal at first… but over time, they can silently sabotage your wealth-building journey. The good news? You’re not powerless.

By staying informed, comparing options, and choosing low-cost investments, you can keep more of your returns and accelerate your progress toward financial freedom.

Get started today by reviewing your portfolio’s fees. Use a tool like Personal Capital or Morningstar to see where your money might be leaking—and then plug those holes.

Thanks for joining us for this deep dive on one of the most overlooked parts of investing. Be sure to check out the Rhodes Brothers YouTube Channel for more insights like this one. Subscribe now and take control of your financial future.

Resource List

Books

- The Bogleheads’ Guide to Investing by Taylor Larimore

- Common Sense on Mutual Funds by John C. Bogle

- The Little Book of Common Sense Investing by John C. Bogle

Podcasts & Courses

- BiggerPockets Money Podcast

- Animal Spirits Podcast

- Coursera: Financial Planning for Young Adults

- Investopedia Academy – Personal Finance for Beginners

Tools & Apps

- Morningstar – Fund analysis and fee comparison

- Personal Capital – Investment fee analyzer + net worth tracker

- Fidelity & Vanguard Tools – Side-by-side fund fee comparison

- M1 Finance – Commission-free investing platform

- Robinhood or SoFi – Beginner-friendly, low-cost brokers

- FeeX – Find hidden fees in 401(k)s and IRAs